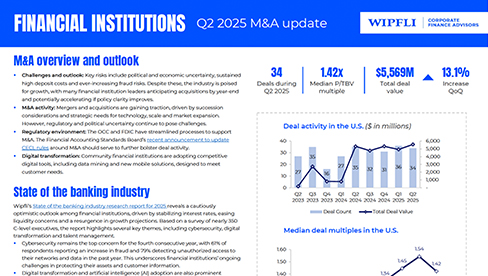

Insights

Helping to preserve a bank’s legacy and its future

After John Connolly — the much-loved president of a fourth-generation, family-owned community bank in western Minnesota — suddenly passed away in 2020, the shareholders and management of West 12 Bancorporation and its wholly owned bank subsidiary, State Bank of Danvers, revisited its strategic plan. They ultimately determined the 121-year-old institution would need to acquire or be acquired to keep up with the ever-changing financial landscape.

Read moreAmperage Electrical Supply, Inc. acquired by Consolidated Electrical Distributors

Vito Pelagio was facing a big decision as he weighed the future of Amperage Electrical Supply, Inc., the business he built and grew as sole owner for 25 years. He had taken the company as far as he believed he could since 1997, with sales rising from $3 million in its first year to more than $110 million in 2022, and his number of employees growing from five to 115. While forever grateful to his mother for helping him secure his first bank loan when he was 26, Pelagio came to realize he needed a new financial strategy beyond taking on new debt to get the firm to the next level. He also realized it was time to turn to outside advisors to help determine and secure the right future for Amperage.

Read moreCloset Works’ $21.5 million sale to The Container Store

When Frank and Tom Happ were ready to sell Closet Works, the Chicago-based company they had bought and transformed over the prior nine years, business was surging. Amid the COVID-19 pandemic, people had hunkered down to create or improve their home organization systems — including closets, pantries, offices, mudrooms and garages — during the home-buying frenzy. There quickly proved to be a lot of interest from buyers in the $23-million company, and the father and son ownership team realized they needed additional help. Wipfli Corporate Finance Advisors worked closely with the Happs to highlight the company’s strengths, negotiate with interested parties and hammer out every detail with The Container Store to get all parties to the closing table.

Read moreSelling two family-owned businesses: Security Door & Hardware Co. and Security Builders Supply Co.

The majority owners of Security Door & Hardware Co. and Security Builders Supply Co., Ron and Russ Benson, had built and grown the two family-held businesses all their lives. Now, ready to retire, the Benson brothers were looking to sell. They hoped to find a new owner who would be a good steward for the businesses, one who would care about their employees and continue the legacy of the two companies. As longtime accounting clients of Wipfli LLP, the owners decided to engage affiliate Wipfli Corporate Finance Advisors LLC (WCF) to advise them through the M&A sale process, ultimately tasking the WCF team with finding the "right" buyer.

Read more